Miran, Fed Independence and Gold

Trump gets his man into the Fed...

BACK to Frankfurt last week for a bunch of meetings over coffee, says Adrian Ash at BullionVault after reporting to readers of the Weekly Update.

Still a lovely city...

...with nice beer but sour cider...

...where the glass tower of the European Central Bank still refuses to look like the same obelisk twice.

But some things have changed. ECB interest rates for one. They've been cut in half over the past 18 months to just 2%.

Then there's the gold price.

"This gold bar belongs to Germany's reserve assets," says a label in the Bundesbank's excellent (and free) Money Museum, describing the 12.5 kilogram lump next to it, refined and cast by Degussa and stamped .9999 fine.

"At a price of 1,000 euro per fine ounce it is worth around 400,000 euro."

Not when I visited last week, however. That fact is now wrong by around 6 years and 220%.

Just an oversight, no doubt. Because the German central bank...by far the largest member of the ECB, yet with only 0.8 of a full vote each year...clearly updates lots of other exhibits for the school trips and random money-obsessives it attracts.

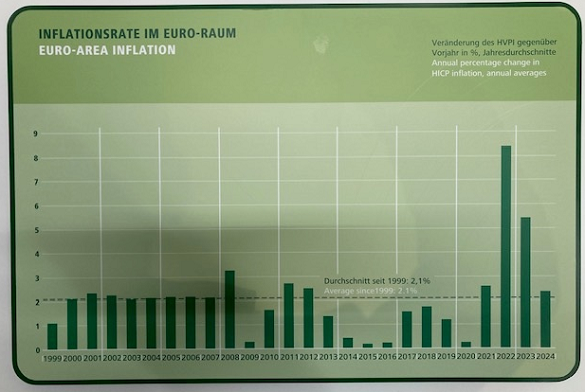

Inflation across the Eurozone, for instance.

"Average since 1999: 2.1%," says this chart...

...running from the year that the Euro currency and monetary union became flesh, and fully updated with the 2024 number.

But all averages lie, and while that 25-year outcome sits pretty much bang on the European Central Bank's 2.0% target, the actual inflation experience across the Eurozone (never mind inside the 20 individual member nations) has been very wide of that mark ever since the global financial crisis struck in 2007.

Is the central bank to blame? Was it to thank for the prior decade of near-perfection?

If so, why?

"The Eurosystem enjoys multiple categories of independence," replies a whole section of the Bundesbank's Museum devoted to that topic.

"Institutional independence means that no national or international institution is permitted to issue instructions to the Eurosystem.

"Aspects of personal independence include the long terms of office of ECB Governing Council members and their protection from arbitrary dismissal."

Reading this stuff on a quick visit to the Museum between meetings last Wednesday felt timely, and weird. Because across the Lowlands and over the ocean, the US Federal Reserve...

...from which Donald Trump had already "fired" one policy maker...

...was holding its first-ever interest rates meeting where a sitting member of the White House would be casting a vote.

Stephen Miran got the job of Fed Governor last Tuesday. He continues to run the President's Council of Economic Advisors. Which is novel.

So too is his approach to the new gig.

Besides voting for a half-point cut last Wednesday...

...twice the cut every other voting Fed member wanted and got...

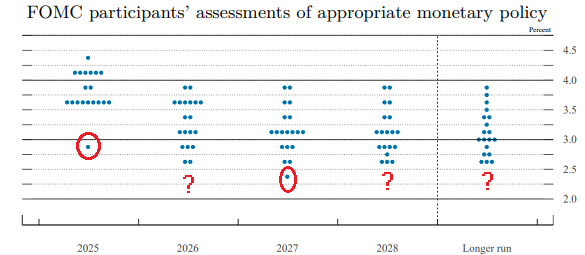

...you can see Miran's longer-term opinions in last week's new chart of Fed members' interest-rate projections.

That's clearly him sitting all by himself at the bottom of end-2025 forecasts, and most probably for the 2027 outlook too.

Who joined him for wanting the cheapest money in 2026 and then long term, we can only guess.

But why not? It's what the boss wants.

"Do you think our economy would be better off with President Trump setting interest rates unilaterally?" Miran was asked by a Democrat lawmaker at his confirmation hearing last week.

"I think," replied the President's man, "that he has had a series of excellent calls on monetary policy over the recent few years."

No kidding! Like in June, when Trump scribbled a note for Fed chairman Jerome Powell saying "You are, as usual, too late. You should lower the rate by a lot!"

Or how about July, when Trump told reporters that "Europe lowered their rate 10 times, we lowered ours none..."

...adding the expert analysis that Powell (whom Trump himself appointed in 2018, believing him to be a "low rates guy") is in fact "a numbskull" a week after calling him a "knucklehead".

Or perhaps Miran meant February, when Trump said that "Interest Rates should be lowered, something which would go hand in hand with upcoming Tariffs!!!"

That third analysis is telling. Because Miran made the same link between White House policy and monetary action just this Monday in his first speech as a Fed governor.

And if you're looking for one single factor behind this week's sudden acceleration in gold and silver's bull markets, you could do a lot worse than read or listen to what he said.

"I love the transparency and detail," says one fan. "Pretty nice to see a Fed governor lay out their thinking so cleanly.

"He'll get blasted by economists for it though because of the aggressive estimates and strong appearance of political bias. Which is a fair critique."

Put another way, "This is batshit insane, no other way to call it," as another analyst said of a speech Miran gave back in April during the chaos following Trump's 'Liberation Day' tariffs announcements.

But that's the point. Up-ending conformity and confounding consensus is exactly how Trump 2.0 operates. And now he's got a team player into the Fed. More of the President's men and women are sure to follow.

R-star, if you must know, is the so-called "neutral" or "natural" rate of interest after you account for inflation...

...a mythical beast which central bankers like to guess and then aim for because, if the economy is running with full employment, it wouldn't restrict or boost the pace of growth.

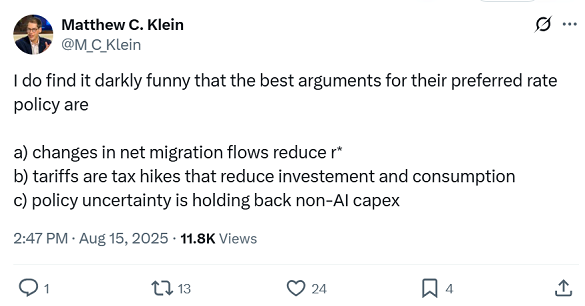

And just like last month's tweet above warned from Matthew Klein, co-author of Trade Wars Are Class Wars...

...the 2020 book which agrees with and pretty much underpins Team Trump's 'destroy the Dollar' aims, even if Klein hates how they're going about it...

...Stephen Miran said in Monday's speech that r* has fallen because of Trump's government policies...

...policies which Miran himself recommended in his so-called 'Mar-a-Lago Accord' published last November...

...and policies which, according to Miran's speech, have reduced the pace of growth and its potential. So the Fed should cut rates, just like Trump always says!

Back in Frankfurt, the Money Museum also draws a clear link between government and central-bank policy. Only this time, it's a warning from history.

"With the outbreak of World War 1 in August 1914," says the Bundesbank, its forerunner the Reichsbank "granted the government unlimited credit to finance the war effort, thus becoming an executive body of the Reich government...

"This sowed the seeds of hyperinflation," the exhibition explains, next to the obligatory black-and-white photos of children playing with stacks of worthless banknotes and old-age pensioners burning cash for heat in 1923.

And then, barely a decade later, amid a deep global depression and deflation, the Nazis seized power.

"They gradually restricted the Reichsbank's independence. The Reichsbank secretly financed the rearmament policy of the Nazi regime. In 1937, it was ruled that the Reichsbank had to report directly to the 'Führer and Reich Chancellor' Adolf Hitler. In 1939, Hitler dismissed six of the eight members of the Directorate of the Reichsbank − including its President, Hjalmar Schacht − for criticising the government's debt policy..."

To be clear, no − none of this means anything close to Stephen Miran's appointment to the Fed being a step towards Dachau or the siege of Leningrad.

Nor should it whitewash the fact that all central banks must and will, in the end, act to support government policy, whether it's the Bank of Japan financing Tokyo's spending during the Lost Decades, or the "independent" Bank of England rushing to QE and near-zero rates after the Brexit referendum...

...or, indeed, the European Central Bank vowing to do "whatever it takes" to keep near-bankrupt member states inside the Euro amid the debt crisis of 2010-2015.

But what Miran's speech does do is to lay bare that the Fed is being captured by Trump, and in a way which, to date, is less like Hitler's seizure of the Reichsbank than, say, how the Central Bank of Turkey was captured by President Erdogan a decade ago, crushing the Lira and driving inflation wild.

The fact that this capture is happening to the world's No.1 central bank, running the world's No.1 reserve and trading currency, only shows what's at stake.

The fact that the Dollar has already sunk faster in 2025 than any year since 2003 only makes the risk of a panic all the greater.

And the fact that gold and silver are soaring against all currencies, not just the Dollar, highlights how confidence in all governments, central banks and consensus politics is being up-ended.

Cue pundits and analysts to note how gold's 2025 jump of 45% in Dollar terms is now the sharpest such rise since 1979. But this comparison misses the big picture...

...first because that year's 133% surge remains an historical outlier, almost twice the gains of gold's next best annual performance...

...and second because gold priced in Dollars matched or beat this year's move three times in a row from 1972 to 1974.

Back then, the Dollar's No.1 status was put in jeopardy by Richard Nixon ending the USA's promise to back its currency with gold, leading to the collapse of the Bretton Woods system and accelerating the 1970s' inflation worldwide.

Nixon was, like Trump, very big on getting the Fed to do as he wished. So if you're looking for a lesson from history right now, and maybe look back 50 years or so to see the harm that the President's Yes-Men can wreak.

Still, at least the stock market keeps going up.

Email us

Email us