No Vaccine Shot for Gold and Silver Fever

Trump 2.0 sees most new bullion buyers since Covid crisis...

With GOLD and SILVER prices rising faster in 2025 than any year since 1979, first-time buying on BullionVault continues to run at levels seen only during financial and economic crises, reports Adrian Ash at the low-cost, world-leading marketplace.

In fact, gold and silver have reacted to the first year of Donald Trump's return to the White House like it's the banking crash or Covid pandemic.

And while there's every chance that the current fever in gold and silver prices will sweat itself out, it's hard to see a cure being discovered any time soon for the long-term bull market in these hard money assets. Certainly not a single shot like the talk of QE tapering hit gold and silver in 2013 or Pfizer's Covid vaccine whacked precious five years ago.

And given next year's geopolitical outlook, plus President Trump's capture of the Federal Reserve, the underlying uptrend in bullion prices looks set to continue.

Over the past 12 months, the surge in new demand at BullionVault − now used by 120,000 people worldwide and caring today for a record $8.0 billion (£6.1bn, €6.9bn) of gold, silver, platinum and palladium − has brought our West London fintech more first-time bullion buyers than any calendar year outside of 2020 or 2011, leaping by 121.7% from 2024.

But the big difference between 2025 and this century's previous surges in new precious metals demand is that Western investors didn't own anywhere near as much bullion going into the financial crisis or Covid pandemic.

So this year's rush has been offset by ongoing profit-taking among existing investors as prices jump ever higher.

Including all existing customers, the number of investors buying gold on BullionVault across November fell 38.8% from October's near-record count, which was second only to March 2020.

The number of gold sellers fell by the same proportion, down 39.3% from October's all-time record. Together, that put the Gold Investor Index − a unique measure of sentiment built solely from actual activity in physical bullion − lower by 3.2 points from October's 56-month high at a 3-month low of 54.7.

Any reading above 50.0 signals more buyers than sellers. As the chart above shows, the Gold Investor Index hit a record high of 71.7 at the peak of the global financial crisis in September 2011, and it hit a decade high of 65.9 as the Covid pandemic and lockdowns went global in March 2020.

March 2024 then saw the Gold Investor Index set an all-time low of 47.5, signalling more sellers than buyers for only the 3rd time in the series' history as a jump in gold prices spurred record-heavy profit-taking without any strong growth in new buyers.

Today is different, with first-time bullion investors running at the strongest ever outside the 2011 or 2020 crises. But prices have moved to fast, new buyers are already seeing strong gains, too. In fact, buying gold any time between January and November would now on average show a US Dollar gain of 23.6% net of all costs using BullionVault (24.3% in GBP, 20.3% in EUR).

Some of 2025's new buyers are happy to bank that profit. They were more likely to sell all or some of their holdings in November than any other vintage of BullionVault users, accounting for 1-in-8 (12.4%) of all gold owners at the start of the month but more than 1/5th (21.2%) of last month's net sellers. That's the strongest ratio of sellers-to-owners among any year's cohort, well over one-third above (36.5%) the next strongest group, 2024.

Overall in tonnage terms last month, gold's new record prices saw investor selling marginally outweigh buying. That cut BullionVault users' total holdings − all secured and insured in specialist, third-party custody in each client's choice of London, New York, Singapore, Toronto or (most popular) Zurich − by 0.1 tonnes (92kg, -0.2%) to the lowest in six months at 43.9 tonnes.

In value terms however, those holdings rose 4.2% across the month in US Dollars (+3.4% in GBP, 3.7% in EUR) to the sixth new month-end record in a row at $5.9bn (£4.4bn, €5.1bn, ¥924bn).

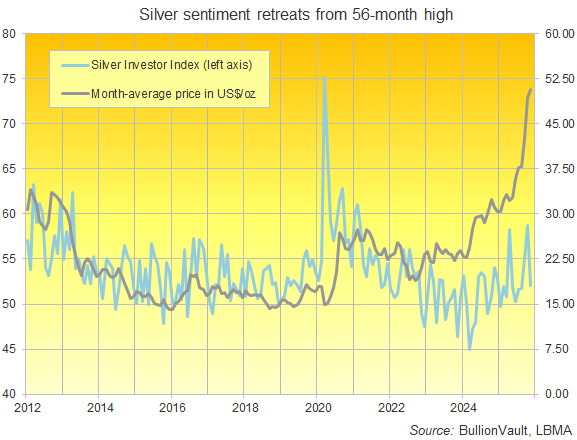

The number of people buying silver meanwhile halved last month from October's 56-month record, dropping by 46.4%.

But the number of sellers also fell, down 23.8% from October's all-time record even as the more industrially-useful precious metal also shot to yet more new record prices.

Together, that cut 6.6 points off the Silver Investor Index, the steepest drop since BullionVault's sentiment index retreated from the Covid Crash spike of early 2020, to give a reading of 52.1, the lowest since August.

The Silver Investor Index set a series high 75.1 in March 2020 as prices sank by nearly 1/5th amid the pandemic's devastating first wave of Covid and lockdowns. It then hit a series low 45.0 in March 2024 as prices rose sharply, spurring record-heavy profit-taking without any strong growth in new buyers.

Priced in Dollars, silver this November averaged more than $50 per Troy ounce, its third new month-average record in a row. That's the longest stretch since silver's 10-month run in 1979.

In tonnage terms, silver's new record prices saw selling outweigh buying for the third month running on BullionVault, trimming users' total holdings by half-a-tonne (555kg, less than 0.1%) to the lowest in four months at 1,153 tonnes.

By value however, those holdings rose 10.1% across the month in US Dollars (+9.4% in GBP, +10.0 in EUR, 12.0% in JPY) to the sixth new all-time record in a row at $2.0bn (£1.5bn, €1.7bn, ¥312bn).

Away from precious metals, meantime − and excluding the nasty break in Bitcoin back below its start-2025 price − there's been no extreme stress in wider financial markets this year. That contrasts with the precious metal surges of summer 2011 or early 2020. Because in 2025, global stock markets have also risen to new all-time highs.

But while the gold and silver fever might just turn out to be a head cold rather than the flu, there are growing fears of a crash in what a growing chorus of analysts and pundits are calling a bubble in AI-related stocks. And looking ahead to 2026, it would be truly different this time if the appeal of rare, physical bullion doesn't rise further should the equity boom turn into bust.

Email us

Email us