Gold Resilient as Mining Stocks Jump

Streamers in particular see revenues rise...

IF THERE's been one constant in 2025, it's gold's ability to attract buyers in an uncertain environment, says Frank Holmes at US Global Investors.

Spot prices had been consolidating in the mid-$3300s after hitting an all-time high of $3500 an ounce in April. The metal's steady performance this summer was fueled by a number of factors, including inflation concerns, a softer US Dollar, central bank demand and the expectation of lower interest rates.

Gold also tends to shine brightest during periods of uncertainty, whether economic, political or geopolitical. This year, that list has been long: renewed tariff skirmishes, questions about the Fed's independence and elevated levels of global debt have all driven investors toward hard assets.

According to the World Gold Council (WGC), gold-backed exchange-traded funds (ETFs) added $3.2 billion in July alone, raising total assets under management (AUM) to $386 billion, a month-end high. Global flows are now on pace for the second-strongest year on record, following 2020.

We have long favored royalty and streaming companies, and their latest quarterly results only reinforce that view. These firms don't own or operate mines themselves. Instead, they provide upfront financing to miners in exchange for the right to purchase a portion of future production − either through royalties or streams − at a fixed, often heavily discounted, price.

This model has several compelling advantages, including lower risk exposure. Royalty and streaming firms have no direct operating costs, meaning they're insulated from rising labor and fuel prices. Their portfolios often span multiple mines and jurisdictions, and they've also demonstrated strong cash flow.

In short, we believe royalty and streaming companies offer a "happy medium" between owning bullion and owning traditional mining equities. They capture much of the upside in a rising gold price environment while providing downside protection during pullbacks.

The June quarter and first half of 2025 were nothing short of spectacular for the big names in the royalty and streaming space.

Franco-Nevada reported record revenue of $369.4 million for the quarter, up 42% year-over-year. Operating cash flow surged 121% to a record $430.3 million, while net income more than doubled to $247.1 million. The company also posted record adjusted EBITDA margins.

Wheaton Precious Metals likewise delivered all-time highs in the second quarter, generating $503 million in revenue and $415 million in operating cash flow. Net earnings came in at $292 million, and the company ended the quarter with $1 billion in cash, no debt and an undrawn $2 billion revolving credit facility.

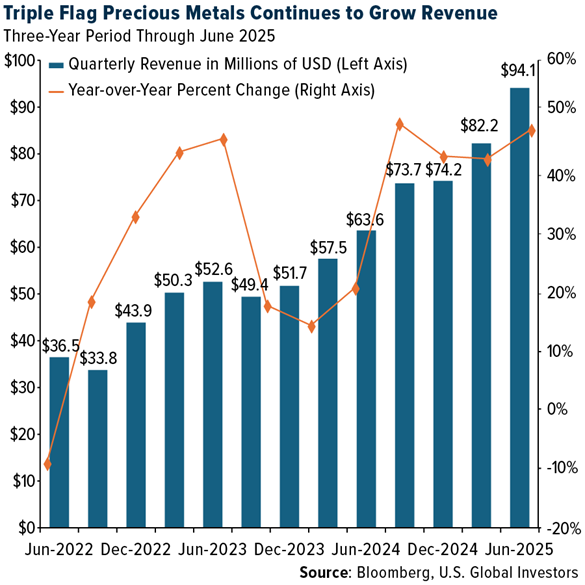

Triple Flag Precious Metals, a relative newcomer compared to its larger peers, posted record operating cash flow per share and announced its fourth consecutive annual 5% dividend increase since its IPO in 2021. Revenues have been growing steadily for the past seven quarters, hitting a new all-time high of $94 million in the June quarter, representing an increase of almost 50% compared to the same quarter in 2024.

These results demonstrate why royalty and streaming companies have been gaining market share in investors' portfolios. They combine the potential for capital appreciation with consistent income, an attractive mix in a yield-starved world.

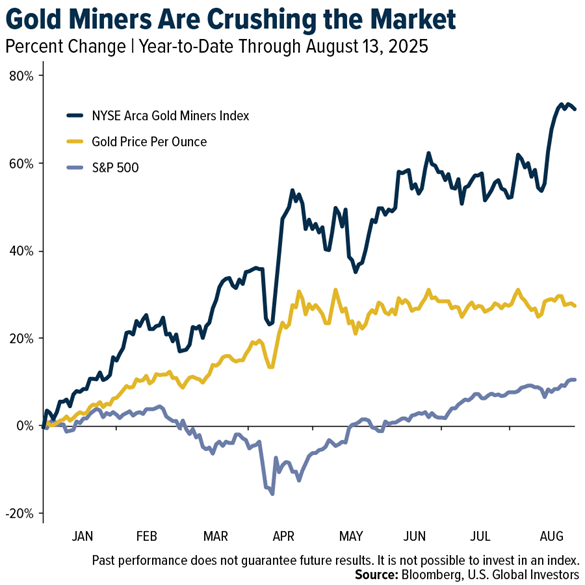

Traditional gold miners are also benefiting from the metal's strength. UBS analysts recently upgraded their outlook on the sector, noting that after years of underperformance, miners are rebuilding investor trust through disciplined capital management.

If gold prices remain steady, UBS sees the potential for increased stock buybacks, accelerated growth projects and more merger and acquisition (M&A) activity. Their top picks include Barrick Gold, Kinross Gold, AngloGold Ashanti, Endeavour Silver and Franco-Nevada.

Returning to the inflation picture, Goldman Sachs has been clear that the tariff burden is shifting from businesses to consumers. Their models suggest that by the fall, about two-thirds of the cost of recent tariffs will be borne directly by US households. This is already showing up in the PPI's services component and could feed into consumer prices later this year.

For investors, this creates a tricky environment. On the one hand, higher inflation readings could prompt the Fed to slow the pace of rate cuts, which might limit gold's upside in the near term.

But on the other hand, persistent inflation − and the potential for policy missteps − reinforces gold's role as a hedge.

History shows that gold has often performed well in periods of negative real interest rates, when inflation outpaced nominal yields. If tariffs and other factors keep inflation elevated while the Fed is easing, we could see that dynamic play out again.

Strong central bank demand, steady ETF inflows and robust free cash flow generation from royalty and streaming companies all point to continued strength in the gold space. For investors looking to participate in this trend, we believe these companies offer an attractive balance of growth potential, income and risk management.

Email us

Email us