India, Gold and the Bond Market's Lords

I command thee: Don't splash my shoes...

KING CANUTE is alive and well, 991 years after he died, writes Adrian Ash in this note first shared last week with readers of BullionVault's Weekly Update.

Or rather, Canute's spirit is thriving today, channelled by politicians and policymakers all over the world.

"You are part of my dominion," Canute shouted at the sea sometime around AD 1030...

...sitting on his throne on a cold English beach in the myth first chronicled a century later.

"The ground that I am seated upon is mine. Nor has anyone disobeyed my orders with impunity.

"Therefore, I order you not to rise onto my land, nor to wet the clothes or body of your lord."

Cue Paula Barker, Labour MP for Liverpool Wavertree.

"Andy is a fantastic politician," she says of wannabee UK prime minister Burnham, currently helping crash the price of government Gilts amid the chaos of Keir Starmer's fast-failing leadership.

Burnham's "progressive policies" will likely mean lots more unfunded spending, she says.

So "the markets will have to fall into line."

"A pretty vertical one!" replies one wag on Twitter of the Government's borrowing costs surging higher Gilt prices sink.

Also shouting at the waves now lapping her shoes is Japan's Finance Minister, Satsuki Katayama.

"The time for taking decisive action" to defend the Yen has arrived, she told reporters at the end of April.

Since then, Tokyo has thrown ¥10 trillion of foreign currency at buying JPY in the forex market, according to Reuters. And its demand for its own currency stalled a drop through the multi-decade low of ¥160 per Dollar.

But the Yen has already started falling again as Tokyo's $63 billion splash of support vanishes into the foam.

"It's hard to expect the move to have a lasting effect on the Yen," says former Bank of Japan governor Haruhiko Kuroda, commentating from near-retirement as a university professor without mentioning his own part in previous Yen-buying campaigns.

"The impact of intervention usually does not last very long."

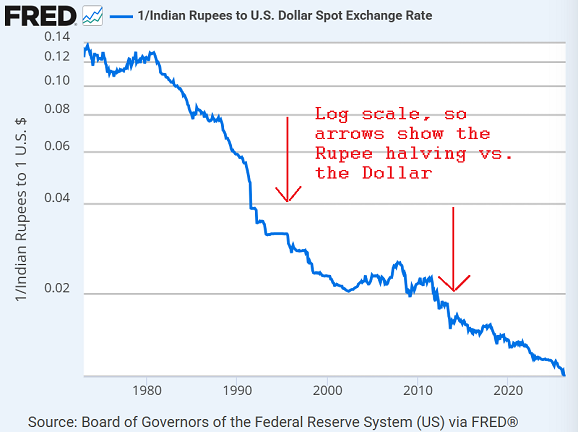

India is also throwing money into the FX market to defend its currency, helping cut the central bank's foreign reserves by 5% from end-February's record worth $728 billion.

India also has an ex-official wise after the fact too, now sniping from the sidelines.

"I believe the RBI should be less interventionist than it tends to be," says former Reserve Bank governor Duvvuri Subbarao...

...under whose rule India sold FX to buy the Rupee during the financial crisis slump of 15 years ago, way back when it was worth $0.02...

...down around half-a-cent from when Subbarao took office in 2008.

"If we want to be a developed economy," he now says, "our market players must learn to manage two-way movement of the Rupee."

But the Rupee only went one way under Subbarao, and it has only gone one way under his successors, too...

...falling this month to barely 1 cent under Sanjay Malhotra.

No wonder Indian citizens buy so much gold.

No wonder Indian governments keep trying to stop them.

India has next-to-no domestic gold mining output. But its demand, while overtaken by China a decade ago, remains the 2nd largest in the world.

Last year that cost the country $72 billion in currency sent abroad to import the stuff, a rise of 25% from the year before and further dragging on India's perennial current account deficit with the rest of the world.

Cue Narendra Modi:

"Patriotism is not only about the willingness to sacrifice one's life on the border," the Prime Minister shouted at a crowd in Hyderabad the Sunday before last.

"In these times, it is about living responsibly and fulfilling our duties to the nation in our daily lives...[and now] we must place great emphasis on saving foreign exchange.

"So for a year, be it for any function, we shouldn't buy gold."

'Function' here means weddings, birthday parties and Diwali. But for Indian households, the true function of gold has become increasingly plain in recent years.

You see, demand is shifting away from jewellery and all the fabrication charges and retail mark-ups it carries, plus steep price discounts when you sell.

Instead, and increasingly like their gold-loving neighbours in China, consumers in India are buying pure investment gold items which carry lower margins and better sell-back prices...

...whether coins, small bars, bullion-backed ETFs on the stock market, or vaulted gold through smartphone apps.

Given gold's religious, cultural and investment appeal, will calling on patriotism cut demand? Will Indians also use less fertilizer, cook with less oil, drive less often and take fewer airflights as Modi also commands?

"In 12 years, he's brought the country to such a pass that the public now has to be told what to buy, what not to buy, where to go, where not to go," says Rahul Gandhi, leader of the opposition Indian National Congress.

That party, of course, repeatedly told consumers not to buy gold when it was last in power. It also yanked gold import duty to untold highs in the dying days of that term in office, ending with Modi's landslide election win of 2014.

India's massive gold industry supported Modi in that victory, backing the new Prime Minister and his BJP party to de-regulate and liberate their market from high duty and also non-tariff barriers such as the Congress Government's disastrous and panicked "80:20" rules of 2013...

...rules so confusing that gold imports to India briefly ground to a halt.

Or rather, the legal import of gold stopped. So-called 'grey market' gold flows flourished. And they continued to boom as the new BJP Government then disappointed India's jewellers and retailers...

...first by failing to reduce gold and silver's high import duty...

...and then by hiking it again and again...

...as well as crushing cash payments with the shock therapy of demonetizing higher-value banknotes at the start of 2017.

Come 2024, the IBJA had given up on Modi and his BJP administration ever giving them a break. So the Government shocked everyone in mid-2024 when it suddenly slashed gold and silver import duty from 15% to 6%.

But then on Wednesday last week, the Finance Ministry reversed that move entirely...

...turning Modi's appeal to patriotism back into the steepest disincentives for precious metals since India was forced into massive economic reforms and liberalization by its current-account crisis of 1991.

How badly will this hit India's gold and silver demand?

Trade association the IBJA projects a 10% drop, and it also warns that smugglers will benefit directly.

The global market has meantime knocked gold $200 lower since India's duty hike, albeit driven far more plainly by the surge in global interest-rate expectations, while silver has lost $5 per ounce to $75 since Modi shouted at the tide.

As for Canute 1,000 years ago, of course he got his feet and legs wet as the waves washed in. That was his point.

"All the inhabitants of the world should know that the power of kings is vain and trivial," he said, moving back up the beach away from the water.

"None is worthy of the name of king but He whose command the heaven, earth and sea obey by eternal laws."

Whether ordained by God (or the gods) or not, India's gold and silver demand look pretty eternal to date.

So too does the law of the universe that using just FX intervention alone never turns the tide for a falling currency...

...as well as the eternal truth that bond-market borrowers cannot choose to ignore the bond market, much less command it to "get in line".

But who cares?

"British politics and the British Parliament can't be run at the behest of the bond markets," says another old-skool Labour MP.

"If the British Government is going to be completely dominated by the bond market, MPs might as well go home."

Okay! Don't forget to take your beach towel and wet clothes with you.

Email us

Email us