Gold Holds US-Iran Deal Rebound as China Price Rallies

The GOLD PRICE held onto a steep rebound from 2-month lows Friday morning, heading for a $15 weekly gain above $4500 per troy ounce as Washington confirmed it's expecting to agree a new ceasefire deal with Iran.

"We're very close to a deal but not there yet," said US vice-president J.D.Vance overnight of the proposed 60-day extension to last month's US-Iran ceasefire, repeatedly tested by military strikes from both sides.

Oil prices held steady, losing 7.5% for the week after US and also Brent crude futures contracts sank ahead of yesterday's news of a possible deal.

Major stock markets rose everywhere except China, with European equities heading for a 4.2% monthly gain despite Nato condemning "Russia's reckless behaviour" after a drone aimed at Ukraine hit an apartment block in neighbouring Romania, a member of the military alliance.

For gold prices to keep rising, "There's a sense that it's going to be a grind," says strategist Nicky Shiels at Swiss bullion refining and finance group MKS Pamp.

"Physical demand continues to be incredibly soft into the summer, and institutional interest has been sidelined, chasing consensual trades like semis [chip manufacturers] and energy.

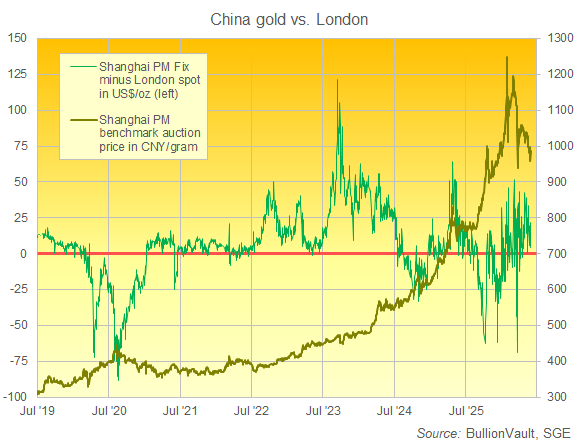

"So without China backstopping − whether its central bank, institutional or retail − it's hard to get genuinely bullish in the short-term.

Shanghai's benchmark gold price today rose 2.8% from Thursday's new 2-month low in Chinese Yuan, edging retail prices back above ¥1,000 per gram just a day after giant bank ICBC led an industry-wide cut in the risk rating on 'gold accumulation plan' smartphone apps, rowing back from the warnings and restrictions made amid China's Christmas chaos in precious metals speculation.

With the Dollar falling to new 3-year lows versus the Yuan, Friday's gold rally put the gap between Shanghai and London prices at $14 per troy ounce, down by 1/3rd from Thursday's 10-session high.

But that premium still offered new imports of bullion − out of gold's central trading and storage hub, into its largest consumer market − twice the long-term average and suggesting solid demand over supply in China.

India in contrast continued to see deep discounts to London gold prices, albeit smaller than the record $200 per ounce reached after mid-May's sudden hike in bullion import duty to 15%, aimed at stemming the country's persistent current account deficit with the rest of the world, now widening on the Iran War's oil-price shock.

"A practical roadmap" to cutting India's gold imports and therefore the CAD is "to substitute a large part by mobilising a small share of India’s estimated 30,000 tonnes of idle gold," says a new policy paper from the India Jewellery & Bullion Association, "held by households and religious institutions."

While the BJP-led Government of Narendra Modi last week denied any plans to demand India's temples sell or loan out their gold, the IBJA has backed those calls, now proposing a "revamped Gold Monetisation Scheme [plus] settling gold metal loans using refined domestic bullion."

India's massive gold loans industry is set for a fresh boom, the Nikkei Asia newspaper reports, as the surge in domestic Rupee gold prices − driven by the hike to import duty − raises the value of gold jewellery and other items which households already own and can pledge against new borrowing.

Silver and platinum showed another weekly loss beneath $75.50 and $1915 respectively after yesterday's stagflationary US economic data, while fellow industrial precious metal palladium held flat at $1372 per ounce on Friday morning.

The price of gold meantime rose over $150 per ounce from Thursday's 9-week low, trading as high as $4530 but still showing a 1.7% loss for the month of May.

Email us

Email us