SPX Blocks Musk's Loss-Making SPCX

Should you buy these record tech IPOs...?

IN CASE you've been living under a rock for the past few months, three of the world's largest and most consequential private companies − SpaceX, Anthropic and OpenAI − are preparing to go public in the same year, writes Frank Holmes at US Global Investors.

Together, they could add nearly $4 trillion in market cap to public markets. Without getting too dramatic, the last time something happened on this scale, the internet was still in its infancy.

I want to help you think through what this could really mean − for your retirement account, and for the indexes you probably own without realizing it.

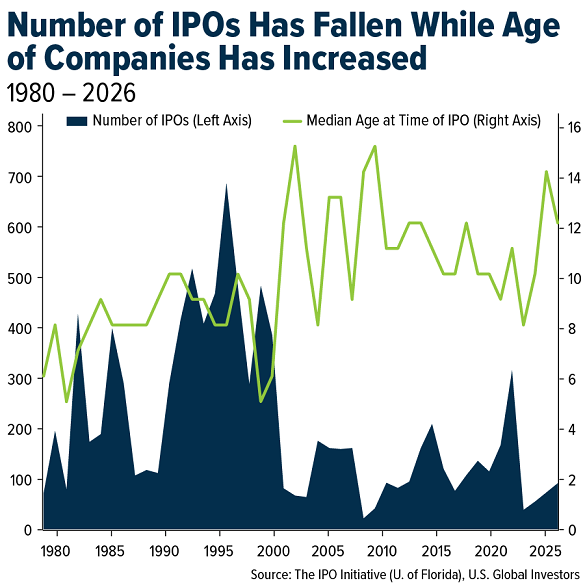

You may remember a time when the initial public offering (IPO) was how companies funded growth. During the dotcom years, firms got listed early, sometimes before they had meaningful revenue, let alone profits.

At the peak in 1995-1996, nearly 700 companies a year went public on US exchanges, according to the IPO Initiative at the University of Florida. The median company was about six or seven years old at the time of its IPO.

That world is gone. Private capital markets have deepened significantly over the past two decades, and venture capital has scaled up. Meanwhile, the regulatory burden on public companies has increased.

Together, these forces have pushed companies toward staying private for longer. Annual IPO counts have fallen sharply from those mid-90s peaks, while the median age of companies the time of listing has roughly doubled, to around 12-14 years.

We're seeing the consequences up close.

SpaceX was founded in 2002. Anthropic was founded in 2021 but has grown faster than virtually any company in venture capital history. In other words, they're mature, scaled businesses, and they're coming to public markets only now, after private markets have funded years of growth.

For investors, this cuts both ways. On the one hand, the risk of early-stage companies is largely behind you. On the other hand, so is a large portion of the potential upside. The early believers in SpaceX, Anthropic and OpenAI have already made their fortunes.

Let's briefly take a look at what's actually on the table with SpaceX and Anthropic.

SpaceX (Nasdaq: SPCX) got a $1.75 trillion valuation in its IPO priced at $135 per share, raising $75 billion, the largest public offering in history.

Before slamming this as unjustified, consider that SpaceX launched 83% of all mass sent into orbit last year. Its Starlink satellite broadband service now has over 12 million paid subscribers. According to the company, Starlink's cumulative network capacity has grown from essentially zero in 2019 to over 600 terabits per second today, with the sharpest acceleration coming in the last 18 months.

As for SpaceX's AI division, Goldman Sachs, the IPO's lead underwriter, is projecting that it will grow roughly 100-fold by 2030, from $3.2 billion to $322 billion. I'd treat that figure as aspirational rather than a forecast, but it tells you what the pitch is based on.

Anthropic's story may be even more remarkable in terms of velocity. The San Francisco-based company's annualized revenue was $4 billion last July, and by year-end, it was $9 billion. By May of this year, it crossed a jaw-dropping $47 billion.

Its valuation, at $965 billion following its most recent round of funding, now exceeds OpenAI's $852 billion. And according to Ramp, which tracks business payment data across tens of thousands of US companies, Anthropic's Claude passed OpenAI's ChatGPT in business adoption for the first time in April. Over 34% of businesses said they subscribed to Claude, compared to 32% for OpenAI.

So why is the company seeking to go public? Anthropic President Daniela Amodei put it bluntly at a tech conference last week: Training AI models is "a very capital-intensive business," and public markets are "very well-suited" to funding that kind of long-cycle investment.

Will you be invested? Most Americans who are saving for retirement are doing so through broad index funds. If you're reading this, you're likely one of them. These products are passive by design, meaning they own what the index tells them to own.

That works mostly smoothly when companies enter the index gradually, at sizes that don't move the needle too much. SpaceX entering at $1.75 trillion is a different matter altogether.

The Nasdaq responded by creating a "fast entry" pathway, allowing companies that rank among the top 40 of its 100 constituents by market cap to get added sooner. Under that provision, SpaceX is expected to be in the Nasdaq 100 just 15 trading days after its June 12 IPO. That means every fund tracking that index will be forced to buy SpaceX. And to fund those purchases, they will have to trim existing positions in Apple, Microsoft, Nvidia and the rest.

The S&P500 took a different path. S&P Dow Jones Indices announced it would not change its rules to fast-track mega-cap IPOs into the SPX index. Under existing methodology, SpaceX doesn't qualify, as it hasn't been public for 12 months, and it reported a $4.28 billion loss in the first quarter of this year. That keeps the company out of the S&P500 for at least a year.

So unlike QQQ ETF investors tracking the Nasdaq, SPX investors holding (for instance) the SPY ETF of S&P500 stocks won't automatically own SPCX, at least not now.

The broader point I'm making is that these massive listings create structural dislocations that are otherwise invisible to most investors. Capital will be reallocated to fund new positions. Rebalancing trades will move prices. And when lockup periods expire − typically 120 to 180 days after the IPO, though SpaceX may follow a staggered approach − there will be additional selling pressure as insiders access liquidity.

None of this makes these IPOs inherently bad investments. It just means the post-IPO price action will be more complex than a simple "up or down" read on the company's fundamentals.

I don't want to dissuade you from buying SpaceX or Anthropic when they list. But I've witnessed a lot of IPO cycles over my decades-long career, and there are some risks you should be aware of.

Thomas Shipp, LPL Financial's Head of Equity Research, looked at roughly 1,500 IPOs from April 1995 through April 2025 on the NYSE and Nasdaq and found that the average one-year return from the first day's close was 10.5%. That sounds decent until you account for the extreme skew in that number.

When Shipp stripped out the occasional extraordinary winner, the median return fell to negative 4.7%. Not only that, but around 60% of the companies in Shipp's sample delivered zero or negative returns over the three years following their IPO. Only around 40% outperformed the S&P500 in year one.

Also consider that the companies bringing these IPOs to market, and the investment banks underwriting them, have every incentive to price them at the upper bound of what investors will pay. The runway for publicly-funded growth has to justify the valuation already baked in the price.

For SpaceX specifically, that means believing not just in Starlink's subscriber trajectory − which is genuinely impressive − but also in technologies that don't exist yet, such as orbital data centers and Mars colonization. I look forward to seeing Elon Musk execute on two these fronts, but for now, the timeline is up in the air.

What we're living through is a once-in-a-generation transfer of private market wealth into public markets. The companies that have defined the last decade of technological progress − satellite communications, artificial intelligence, space infrastructure − are finally arriving on exchanges where ordinary investors can own them.

If you're thinking of participating, I hope you approach them the way you would any concentrated, high-conviction bet.

Email us

Email us