Silver and Gold Fall as Governments Rush to Curb Iran War's Oil Price Shock

SILVER and GOLD PRICES erased this week's prior gains on Wednesday, falling as energy costs rose despite Asian and Western governments trying to curb the oil price shock from the new Middle East war.

With 1 Troy ounce of silver falling back below US crude oil prices per barrel, Austria and Germany joined South Korea in proposing a cap on how often petrol-pump prices can be raised, while several Asian nations restricted air-con use in government offices, and Pakistan ordered a 4-day work-week.

The International Energy Agency then announced the release of 400 million barrels of oil from its member nations' strategic reserves, more than twice the quantity released from IEA stockpiles in response to Russia's invasion of Ukraine in 2022.

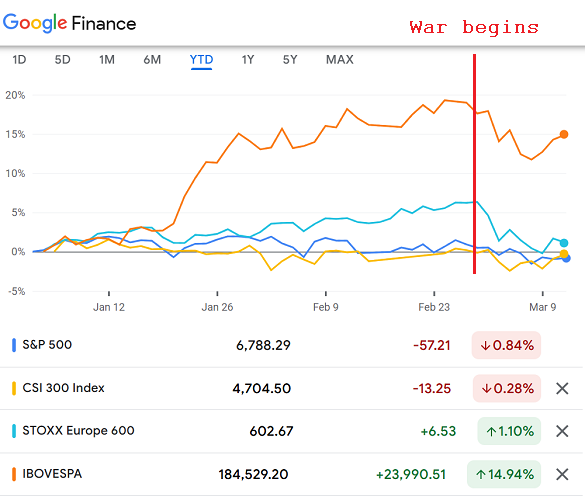

New York's stock market opened the day flat following the IEA announcement, trading around 1.5% lower since US-Israeli airstrikes on Iran began this conflict at the end of February.

Shanghai's CSI300 has traded virtually unchanged meantime, but the EuroStoxx 600 index has erased almost all of a 6.3% year-to-date gain, losing its prior outperformance over China and the USA.

Equities across Latin America − isolated so far from the Middle East war and its impact on Euro-Asian oil supplies − have kept 70% of their near 1/5th gain in Euro terms on the Stoxx index of Latam shares, led by Brazil's Bovespa Index and with 4 energy producers in the 10 largest stocks.

"Once the war ends, we think that gold prices could drop back to their pre-war level of around $4600," says a note from analyst Bernard Dahdah at French bank Natixis, estimating that "the total impact of market expectation and reaction to the war has been as much as $750/oz.

"That said, should war drag on for more than two weeks, we do not think that gold prices will continue to go sideways [thanks to] the inflationary impact that higher energy prices could have on the global economy."

Trading as low as $5153 and $84.50 per Troy ounce, gold and silver prices fell 1.6% and 5.3% respectively on Wednesday from yesterday's rally to 1-week highs.

Base metals copper and nickel also fell from this week's earlier rally.

"There's no plug for a hole this large," says Canadian brokerage TD Securities' commodities strategist Daniel Ghali of the damage done to global oil flows by Iran attacking tankers passing through the Strait of Hormuz.

"Of the ships we have identified passing through the Strait of Hormuz, many have links to Iran, China or Russia," says UK Sky News' open-source intelligence editor Adam Parker.

China's crude oil imports rose 15.8% per year during January and February, led by higher refining demand plus continued stockpiling which should now help insulate the giant Asian economy from the Hormuz disruption to east-bound tankers.

Oil refineries in India have bought 30 million barrels of Russian oil since the US Treasury last week suspended the secondary sanctions it imposed over the Kremlin's ongoing war in Ukraine.

But India's largest bank is refusing to process payments for Russian crude, Bloomberg reports, amid uncertainty over how long the suspension will last.

Over in the bond market. longer-term interest rates had slipped overnight in Asia as local stock markets rose.

But borrowing costs for Western governments then rose again as energy prices rallied, with benchmark yields nearing 1-month highs on US Treasury debt, the highest since last autumn for the UK and Italy, and approaching the top of the past 2.5 years' multi-decade highs for Germany and France.

Brent crude oil rallied above $90 per barrel but held almost 25% below Monday's 44-month high near $120.

Russia's Urals Blend benchmark rallied hard to $88 per barrel after sinking by 1/3rd from Monday's 4-year high above $100.

European natural gas prices also rallied but held 1/8th below Monday's peak on Dutch TTF April futures.

Email us

Email us